New Jersey Property Taxes & Your Mortgage

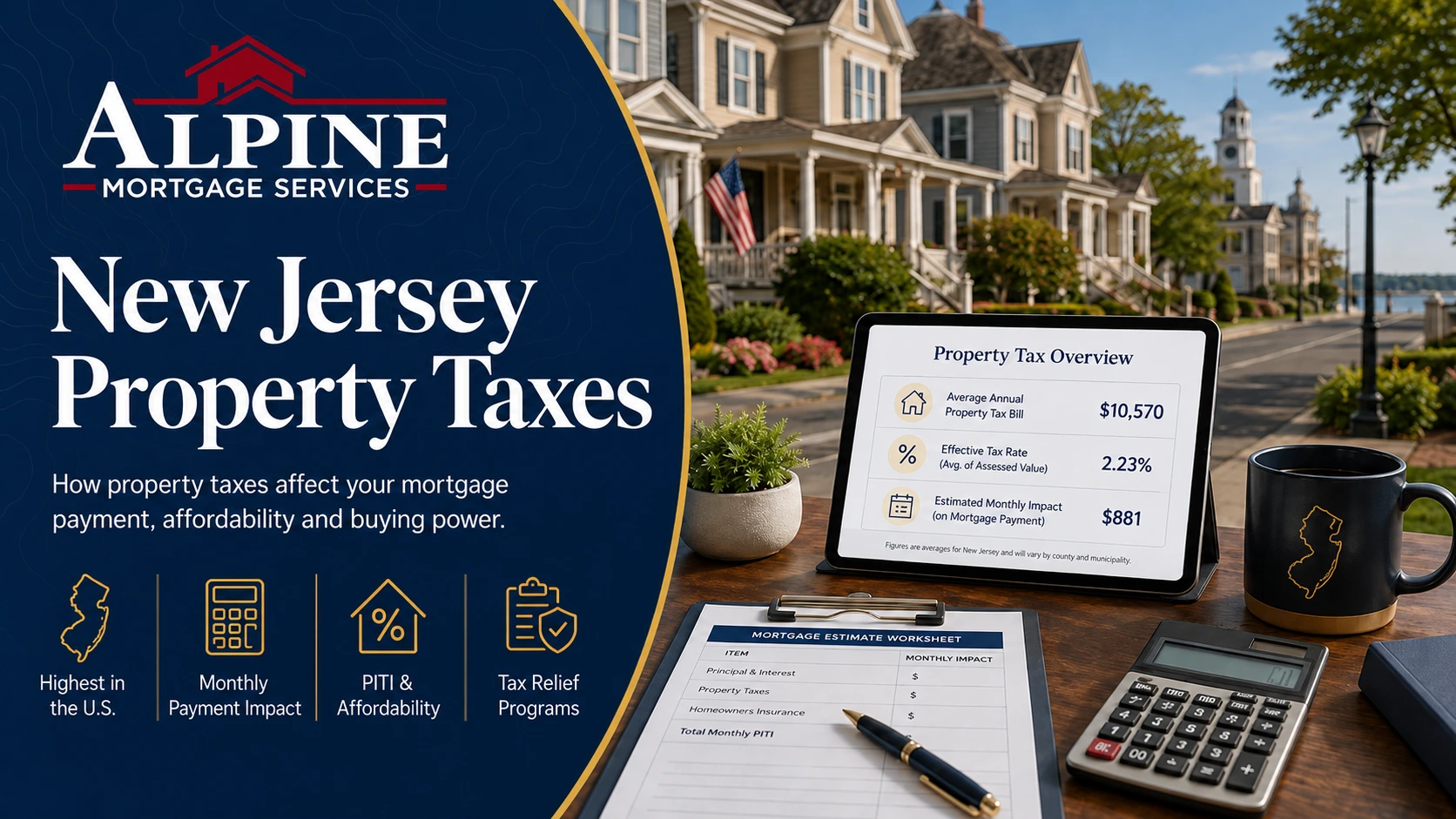

New Jersey has the highest property taxes in the United States. The statewide average property tax bill exceeded $10,000 for the first time in 2025 reaching $10,570. For homebuyers, property taxes directly impact how much home you can afford and whether you'll qualify for your mortgage.

This guide explains how NJ property taxes affect your mortgage qualification, which towns have the highest and lowest rates and how to factor taxes into your homebuying strategy.

Why Property Taxes Matter More in New Jersey

When you apply for a mortgage, your lender calculates your debt-to-income ratio (DTI): the percentage of your gross monthly income that goes toward debt payments. Property taxes are included in this calculation as part of your monthly housing payment (PITI: Principal, Interest, Taxes, Insurance). In most states, property taxes add a few hundred dollars to your monthly payment. In New Jersey, they can add $800 to $1,500+ per month sometimes exceeding your principal and interest payment.

Here's how property taxes impact mortgage qualification for a buyer with $10,000 gross monthly income:

| Scenario | Monthly P&I | Monthly Taxes | Insurance | Total PITI | Front-End DTI |

|---|---|---|---|---|---|

| Low Tax State (1% effective rate on $500K) |

$2,398 | $417 | $150 | $2,965 | 29.6% |

| NJ Low Tax Town (1.5% rate on $500K) |

$2,398 | $625 | $150 | $3,173 | 31.7% |

| NJ Average Town (2.2% rate on $500K) |

$2,398 | $917 | $150 | $3,465 | 34.6% |

| NJ High Tax Town (3.0% rate on $500K) |

$2,398 | $1,250 | $150 | $3,798 | 38.0% |

Assumes 6% rate, 30 year fixed, 20% down on $625,000 purchase

The takeaway: The same buyer buying the same priced home has a DTI that varies by nearly 9 percentage points depending on which NJ town they choose. For buyers near DTI limits this can mean the difference between approval and denial.

How This Reduces Your Buying Power

Because property taxes consume more of your allowable DTI in New Jersey you can borrow less than a similarly situated buyer in a lower tax state. A buyer who could afford a $600,000 home in Pennsylvania might only qualify for $500,000 in a high tax NJ town not because of income but because of taxes.

Pro Tip: When we prequalify you for a mortgage, we use actual tax data from the specific property you're considering and not estimates. Always ask about property taxes early in your home search.

New Jersey Property Taxes: The Numbers

Statewide Statistics (2025)

| Metric | New Jersey | National Average | Difference |

|---|---|---|---|

| Average Property Tax Bill | $10,570 | $3,500 | 3x higher |

| Effective Tax Rate | 2.23% | 0.89% | 2.5x higher |

| Median Home Value | $405,000 | $350,000 | 16% higher |

Sources: NJ Department of Community Affairs, Tax Foundation, SmartAsset

Property Taxes by County

| County | Avg. Tax Bill | Effective Rate | Avg. Home Value |

|---|---|---|---|

| Essex | $14,460 | 2.5%+ | $494,335 |

| Bergen | $12,500+ | 1.8-2.2% | $625,000+ |

| Morris | $11,500+ | 2.0% | $600,000+ |

| Union | $11,000+ | 2.1% | $500,000+ |

| Monmouth | $10,000 | 1.48% | $674,100 |

| Hudson | $9,752 | 1.69% | $577,000 |

| Middlesex | $9,427 | 1.82% | $518,000 |

| Camden | $7,500 | ~2.3% | $325,000 |

| Ocean | $6,500 | 1.2% | $475,000 |

| Cumberland | $3,744 | 2.13% | $175,700 |

Source: NJ Department of Community Affairs, SmartAsset 2025

Highest and Lowest Property Tax Towns in NJ

Highest Average Tax Bills (2025)

| Municipality | County | Avg. Tax Bill | Effective Rate |

|---|---|---|---|

| Summit | Union | $19,697 | 1.8% |

| Chatham Township | Morris | $18,370 | 2.0% |

| Weehawken | Hudson | $17,793 | 1.87% |

| Haddonfield | Camden | $17,761 | 2.5% |

| Millburn | Essex | $17,000+ | 1.7% |

Lowest Property Tax Rates (Effective Rate)

| Municipality | County | Effective Rate | Notes |

|---|---|---|---|

| Teterboro | Bergen | 0.60% | Industrial/commercial, minimal residential |

| Walpack Township | Sussex | 0.63% | Rural, limited services |

| Tavistock | Camden | 0.88% | Tiny, exclusive community |

| Cape May Point | Cape May | 0.70% | Beach community |

| Longport | Atlantic | 0.85% | Shore community |

Lower Tax Options with Good Services

The lowest tax towns are often impractical (no services, rural, etc.). Here are municipalities with reasonable tax rates and good schools/services:

- Cranbury Township (Middlesex): 1.9% rate, excellent schools

- Toms River (Ocean): 1.2% rate, good services, shore access

- Monroe Township (Middlesex): 1.8% rate, 46,000 residents, parks/recreation

- Kearny (Hudson): 1.5-1.8% rate, NYC access

- Mount Laurel (Burlington): 1.6% rate, good schools, corporate presence

How Property Taxes Affect Your Mortgage Qualification

The DTI Calculation

Lenders calculate two types of debt-to-income ratios:

Front End DTI (Housing Ratio): Your monthly housing payment (PITI) divided by gross monthly income. Lenders typically want this below 31-45%.

Back End DTI (Total Debt Ratio): All monthly debt payments (housing + car loans + student loans + credit cards + other) divided by gross income. Lenders typically want this below 45-50%.

Property taxes are included in both calculations. Higher taxes = higher DTI = reduced buying power.

Qualifying With High Property Taxes

If you're buying in a high tax town, here are strategies to improve qualification:

- Increase your down payment: Lower loan amount = lower P&I = more room for taxes in your DTI

- Pay off other debts: Eliminating a car payment or credit card balance frees DTI capacity

- Consider a lower priced home: Lower purchase price = lower taxes (and lower P&I)

- Look at neighboring towns: A few miles can mean thousands in annual tax savings

What Lenders Use for Tax Estimates

During prequalification, lenders may estimate property taxes. But when you're under contract on a specific property, we use actual tax data:

- Current year's tax bill from public records

- If recently reassessed, the new assessment value

- For new construction estimated taxes based on projected assessment

Warning: If you're buying from a long time owner with a very low assessment, taxes may increase significantly after your purchase triggers reassessment. We can help you estimate the potential increase.

New Jersey Property Tax Relief Programs

New Jersey offers several programs to reduce property tax burden. In 2026, these are being consolidated into a single application (Form PAS-1) for easier filing.

ANCHOR (Affordable NJ Communities for Homeowners and Renters)

| Who Qualifies | Benefit Amount |

|---|---|

| Homeowners (income up to $250,000) | $1,000 - $1,500+ |

| Renters (income up to $150,000) | $450+ |

ANCHOR is the broadest program, covering most NJ homeowners regardless of age. Benefits are paid as a check or direct deposit, not as a credit to your tax bill.

Senior Freeze (Property Tax Reimbursement)

For homeowners 65+ or receiving Social Security Disability. "Freezes" your property tax at a base year amount and the state reimburses you for any increases above that level.

- Eligibility: Age 65+ (or disabled), income limits apply

- Benefit: Reimbursement for tax increases since your base year

- How it works: Your taxes can still increase, but the state pays the difference

Stay NJ (New for 2024-2025)

New program providing significant relief for seniors:

- Eligibility: Homeowners 65+, income under $500,000

- Benefit: 50% of property taxes reimbursed up to $6,500 (2025 cap, increasing to $13,000 max)

- Payment: Quarterly installments

Stay NJ is calculated after ANCHOR and Senior Freeze benefits so eligible seniors can potentially stack all three programs.

Other Programs

- Veterans Exemption: $250 annual deduction for honorably discharged veterans

- Disabled Veterans: Up to 100% exemption depending on disability rating

- Property Tax Deduction for Seniors/Disabled: $250 deduction if income under $10,000

How to Apply

Most programs now use the combined PAS-1 application, available online at propertytaxreliefapp.nj.gov or by mail. Filing deadline for 2025 applications is November 2, 2026.

Appealing Your Property Taxes

If you believe your property is over assessed you can appeal. Successful appeals can reduce your annual tax bill by 10-25%.

When to Appeal

- Your assessed value is higher than recent comparable sales

- Your assessment increased significantly after a revaluation

- Similar homes in your area have lower assessments

- Your property has condition issues not reflected in the assessment

Appeal Deadlines

Standard deadline: April 1 (or 45 days from Assessment Notice mailing, whichever is later)

Monmouth County: Different timeline due to annual reassessment program. Check county website.

The Appeal Process

- Gather comparable sales data (similar homes sold within past year)

- File appeal with your County Board of Taxation

- Attend hearing (informal, usually 15-20 minutes)

- Receive decision (typically within 3 months)

- If unsuccessful, can appeal to NJ Tax Court

Pro Tip: Many homeowners hire tax appeal attorneys or consultants who work on contingency (typically 25-50% of first year savings). This can be worthwhile if your potential savings are significant.

The SALT Cap & Federal Tax Implications

The federal $10,000 cap on State and Local Tax (SALT) deductions significantly impacts New Jersey homeowners. If your property taxes alone exceed $10,000, which they do for more than half of NJ homeowners, you cannot fully deduct them on your federal return.

Example Impact

Homeowner with $12,000 property taxes + $8,000 state income taxes:

- Total SALT: $20,000

- SALT Cap: $10,000

- Lost deduction: $10,000

- Tax impact (24% bracket): $2,400 additional federal tax

This effectively raises the true cost of high NJ property taxes even further.

Property Tax Strategies for NJ Homebuyers

Before You Start Your Search

- Get prequalified with realistic tax estimates. Don't use optimistic numbers. Assume taxes will be at or above average for your target area.

- Research towns, not just neighborhoods. Municipal boundaries determine your tax bill. Two homes across the street can have vastly different taxes if they're in different towns.

- Use actual tax data. Check any property's current taxes at your county assessor's website or ask your real estate agent to pull the data.

During Your Search

- Compare total monthly cost. A $500K home with $15K/year taxes costs more monthly than a $550K home with $8K/year taxes.

- Ask about recent assessments. If the town recently revalued current taxes are more reliable. If not, they may increase.

- Consider future trajectory. Towns with aging infrastructure or growing school budgets may see rising taxes.

Making Your Decision

Property taxes should be a primary consideration and not an afterthought when choosing where to buy in New Jersey. The right town choice can save you $5,000-$10,000+ annually which over a decade adds up to $50,000-$100,000 or more.

Steven Parangi is a licensed mortgage loan originator (NMLS #76024) and attorney with over 20 years of experience in residential home lending. As the founder of Alpine Mortgage, Steven works directly with borrowers to review their mortgage options and assist them throughout the home financing process. Content published on AlpineBanker.com is reviewed regularly by Steven to reflect current lending guidelines and market conditions.

View full author profile →NJ Property Taxes FAQs

Yes. Property taxes are included in your monthly housing payment (PITI), which is used to calculate your debt-to-income ratio. Higher taxes mean less room for principal and interest, which reduces your maximum loan amount.

New Jersey funds local services almost entirely through property taxes rather than state income or sales tax revenue. The state's 565 municipalities each set their own budgets leading to fragmented and expensive service delivery. Additionally, NJ has strong public schools, extensive municipal services and high median incomes which contribute to higher tax levies.

Possibly. If you're buying from a long time owner with an outdated assessment the town may reassess after your purchase. Additionally, towns can increase tax rates to fund budget increases. However, you won't face surprise reassessment solely due to a sale. NJ doesn't have a "sale triggered" reassessment like some states.

You can deduct up to $10,000 in combined state and local taxes (SALT), including property taxes and state income taxes. For many NJ homeowners, property taxes alone exceed this cap meaning you cannot fully deduct them.